Oil demand decreased in 2020 during the pandemic as a result of the severe economic slump that caused the price of oil to fall for the first time below zero. Since then, a robust post-lockdown economic rebound has caused oil prices to surge to over $100 per barrel.

In addition, escalating geopolitical tensions in the Middle East and between Russia and Ukraine are exacerbating supply issues. Rising prices and worries about an economic recovery are a result of this. One of the most significant commodities in the world, oil accounts for around 3% of GDP. Petroleum products are used in a wide range of items, in addition to PPE, plastics, chemicals, and fertilizers.

The world is moving away from oil. It’s a necessary evil that’s slowly being replaced by renewable energy sources. The problem is, that the transition is taking longer than anticipated. In the meantime, the demand for oil continues to increase while the supply dwindles. This has caused the price of oil to skyrocket, and it’s no longer affordable for many people.

The low price elasticity of oil consumption may someday alter due to the worldwide push towards sustainability, but in the meantime, people are struggling to pay for necessities like food and healthcare. Of course, there are lots of ways to get money, no faxing payday loans are one way to help cover unexpected expenses, but they should not be relied on as a long-term solution to the problem of high oil prices.

The Rising Cost Of Oil

Currently, a barrel of oil costs approximately $100. The oil market seems to have just one constant, which is change and volatility. But it’s generally reasonable to state that the top three causes are as follows:

Oil Consumption Is Boosted By Rapid Economic Expansion

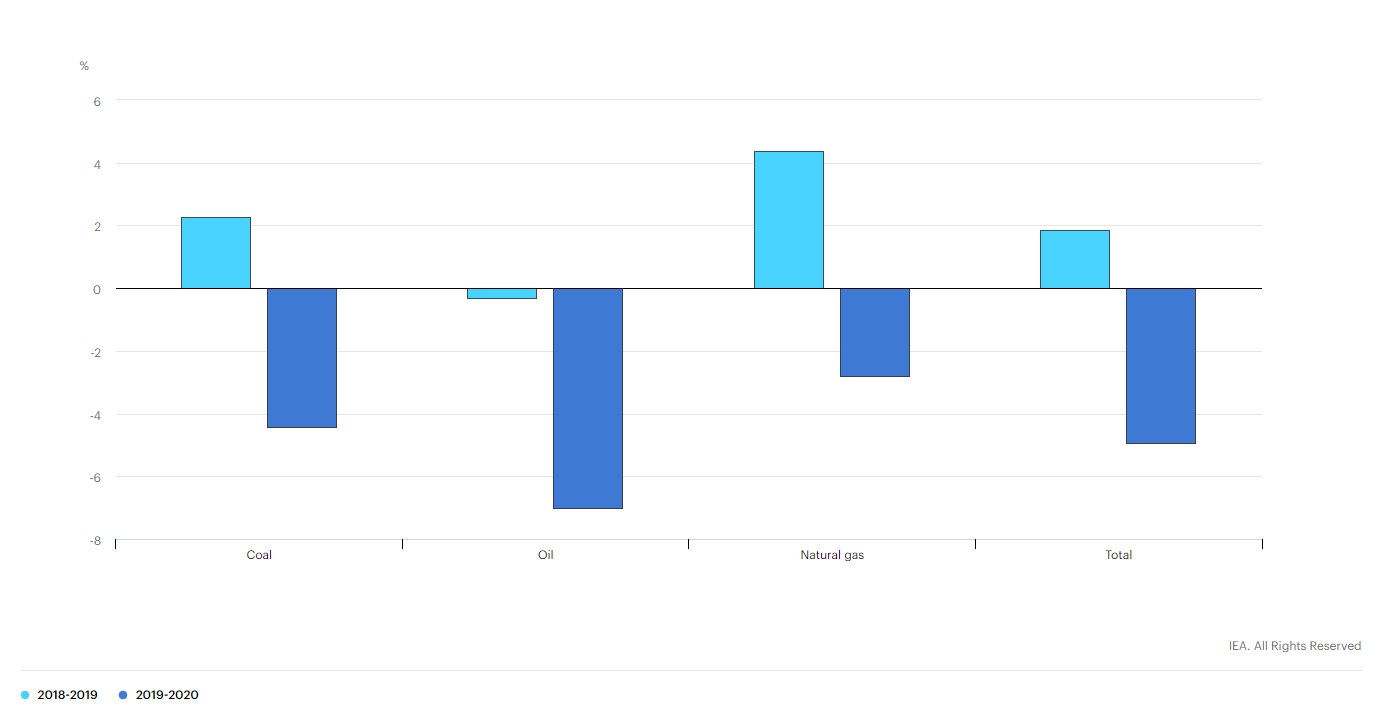

When COVID-19 first started two years ago, there was a decline in both the demand for oil and economic activity. Although producers have been changing their output levels, there isn’t much that can be done without damaging resources or capital. Additionally, storage space is restricted.

In addition, the severity and duration of the impending economic catastrophe were also unknown. Oil prices have fallen to very low levels that have not been witnessed in decades due to these combined circumstances. Even for a little time, oil prices fell to a negative $40 level.

This challenging time persisted for many months. An unexpected economic rebound that followed this led to an increase in demand for oil and petroleum-based goods. At this stage, oil demand is predicted to have reached or surpassed pre-pandemic levels.

Limited Oil Supply as a Result of Conservative Capital Allocation And Lengthy Investment Cycles

The rising demand could not be completely satisfied by the offer. Although OPEC has taken its time increasing oil output, it also has little spare capacity and is probably taking caution to avoid oversaturating the market once again.

The production of oil also has relatively lengthy investment cycles in addition to spare capacity. It may take up to 10 years from the moment when the availability of the resources is certified until the first production begins. Although some non-traditional sources have a smaller output, they may generate more quickly.

Additionally, every manufacturer carefully distributes money. They first gained knowledge from a flooded market when oil prices fell to a negative $40. Second, and possibly more significantly, there is intense pressure on the sector to forego the development of new resources, hold off on or scale down investment in maintaining and expanding output, and shift funds to green investments.

Tensions in Geopolitics

Increased Middle East instability and geopolitical tensions between Russia and Ukraine are making the oil market more uneasy. Higher oil prices could not have as much of an impact on the world economy as conventional economic theory would predict since it is a complicated system.

Here are the top three explanations of why the price of oil affects the world market.

The first factor that makes oil prices important to the world economy is that it stimulates it. Oil is essential to the economy of the globe. For many years, rising oil consumption has outpaced increases in oil production and surplus capacity. Rapid global population growth has driven down manufacturing and transportation costs, boosting the economy. However, the drawback of low energy costs is that they may harm domestic oil employees and American oil corporations.

Second, a country’s economic structure affects how oil prices affect it. Oil-exporting nations are particularly susceptible to changes in the world commodities market. This is particularly true for nations where a large portion of their industrial output uses fossil fuels. Additionally, the consequences of changes in oil prices may be amplified by the dollar exchange rate and current inflationary pressures. As a consequence, a rise in oil prices may benefit countries that export oil while a fall in oil prices may harm those that import oil.

Additionally, the cost of production in the United States is directly impacted by the price of oil. Gasoline prices, which are a significant factor in transportation, have a direct relationship with economic expansion. Consequently, a decline in oil prices will result in less expensive travel. The industrial industry, which is highly reliant on oil exports, may also be impacted.

Why Does the Global Economy Care About Oil Prices?

Oil is the primary energy source for the world economy, which makes up about 4% of the total. It becomes a precious commodity as a result. Its consumption and economic activity are connected. The cost of other commodities is likewise influenced by the price of oil. Higher global demand for petroleum will increase the price of other commodities in addition to limiting the supply. Gas prices will decline if supply and demand both fall.

Oil prices are influenced by both the price of oil and the economic activity in non-OECD regions. Oil consumption is impacted by a nation’s economic development, which in turn impacts the cost of other commodities and services. It may result in increased pricing in the US during economic downturns. Even while this pattern mostly affects poor nations, it does have an impact on the cost of other commodities, such as oil.

Oil price increases can hamper the economy. It may therefore raise the price of other products and services. The supply curve for products and services that depend on the availability of oil might change as a result of rising oil prices. It’s crucial to keep in mind that the price of oil is directly correlated with the nation’s present economic situation.

The demand for these products and services will increase if the price of oil continues to climb. Low pricing, on the other hand, might raise the price of other products and services. If prices stay high, economic activity will stagnate and maybe even decline.

The price of oil is impacted by shifting economic circumstances. For instance, the percentage of manufacturing industries rises while overall oil consumption declines in emerging nations. The demand for oil rises as a result. The need for food and energy may increase as a result of the increasing oil costs. These elements ultimately have an impact on crude oil’s price. Long-term, the rising oil price will raise the cost of goods in emerging nations.