When it comes to personal finance, navigating the world of budgeting, investing, and saving money can be intimidating. You know you need to manage your finances properly but aren’t sure how to start.

Fortunately for you, this blog post aims to demystify the personal financial landscape by providing readers with an easy-to-understand overview of essential concepts related to money management.

This guide provides actionable tips that will set anyone on a path toward better financial health, no matter their level of experience or starting point. So if you are ready to take control of your own finances so that in the future, you do not have to ask the following question as how to build credit after bankruptcy, read on!

How Crucial Is Personal Finance?

It might be daunting to deal with money. In fact, 80% of Americans say they delay making financial decisions, and 35% of those who do so say it’s because they feel overburdened just thinking about it.

Take each component, however, one facet at a time. Get that down, then go. In order to manage your lifestyle security, there are four crucial stages that personal finance must address:

1) Earning income.

2) Spending less.

3) Increasing wealth.

4) Safeguarding property.

Throughout your life, these goals may conflict. You have already completed some of the fundamentals. When you go on to another work intended to optimize your money, knowing that might give you confidence.

Lower Your Monthly Bills

Cutting your monthly spending is one of the simplest ways to gain control of your money.

While you might not be able to reduce recurring expenses, such as rent or car payments, without making substantial lifestyle adjustments, you can reduce recurring expenses, such as clothing or entertainment, by being flexible and frugal.

To save your energy bills, you may, for instance, use less power, pick a different life or home insurance company, or shop for your groceries at bulk discounts.

Settling Credit Card and Loan Debt

The debt with the highest interest rate should be paid off first if you have personal loans or credit card debt. Credit cards are one example. The poll found that nearly 2 out of 5 Americans (38%) are likely to postpone establishing a new bank account or selecting a new bank.

Store cards often have the highest interest rates, whereas personal bank loans typically have lower interest rates than credit or store cards. Making ensuring you adhere to the terms of your agreements is crucial.

Therefore, even if you’re concentrating on paying off another obligation, you still need to pay at least the minimum balance on all credit cards and your monthly loan payments.

Avoid Dining Out

You want to manage your monthly variable costs, but you don’t know where to start. Don’t order takeout as often. Even if it’s acceptable to treat yourself occasionally to a fine restaurant, you could end up saving money if you start cooking at home or bring a lunch to work instead of eating out every day.

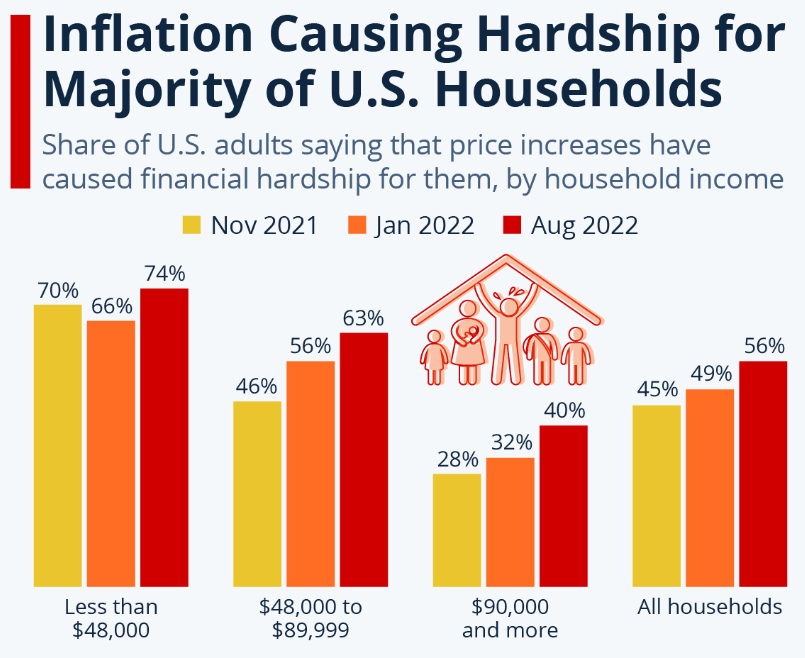

However, the effects of inflation have even reached high-income households, as 40% of individuals with household incomes over $90,000 now report experiencing financial hardship due to inflation, up from only 29% in November 2021.

Source: Statista.com

Make at least one meal every week at home to start. Beginning the next week, start taking lunches to work. The amount of money you can genuinely save could astound you. By brown-bagging it, you may save $1,300 yearly or more than $50,000 throughout a 40-year career.

Spend Some Time-Saving Money, but Do It.

Establish a savings account for emergencies so that you may use it when they arise. Even with modest contributions, you can avoid difficult circumstances where you might have to take out high-interest loans or run the risk of not being able to make your payments on time.

To improve your ability to survive financially in the case of a job loss, you should also make general savings contributions. Increase this fund and encourage the practice of saving money by using automated donations.

Spend Less Than You Earn and Receive the Compensation You Deserve

Even though it appears simple, many people struggle to adhere to the first guideline. You should be aware of the market worth of your position by evaluating your skills, output, job duties, contribution to the company, and the going rate for what you do both inside and outside the business. Even a $1,000 yearly wage drop may have a significant cumulative effect throughout your career.

No matter how much or how little money you make, you’ll never be able to get ahead if you spend more than you make. A modest cost-cutting effort may provide savings in various areas since spending less money is frequently simpler than earning more. Additionally, significant sacrifices are not always necessary.

Set Both Immediate and Long-Term Objectives

It takes time and effort to build financial stability. You’ll have certain money-related goals that you want to accomplish as soon as possible. Other objectives may have start dates that are ten or more years away yet call for commencing as soon as possible.

Making a comprehensive list of all your objectives is a wise first move. When you know exactly what you want to accomplish, it is usually simpler to plan a path of action.

You decide whether your immediate and long-term objectives list will be written down or entered into a spreadsheet. Be careful to allow yourself some alone so you can consider it.

Your Student Loans: Manage Them

If you don’t take action to pay off your student loans, you might be burdened with debt for years. To determine whether you are eligible for student loan forgiveness programs, whether to refinance or combine them, or whether to include them in a debt repayment plan, you need to analyze your situation, determine the value of each option and make a choice. It’s a great idea to take charge of your student debts immediately away to improve your financial situation.

Conclusion

To enhance your personal finances, you don’t require a raise in income or a windfall from a family member. Many people find that improving their money management skills is all it takes to cut back on their spending, increase their capacity to invest, save and reach previously unattainable financial objectives.